I recently read an article about financial advice you can fit on an index card. I’m going to share it with you, but it got me thinking about what financial advice I would put on an index card, and a few seconds later, I had filled mine up. I decided not to refine it or rewrite it but share it with you and tell you why each of those made it onto my initial list (plus a bonus tip not written on the card!) Also, I didn’t have an index card, but a pocket-sized Moleskine page worked just fine.

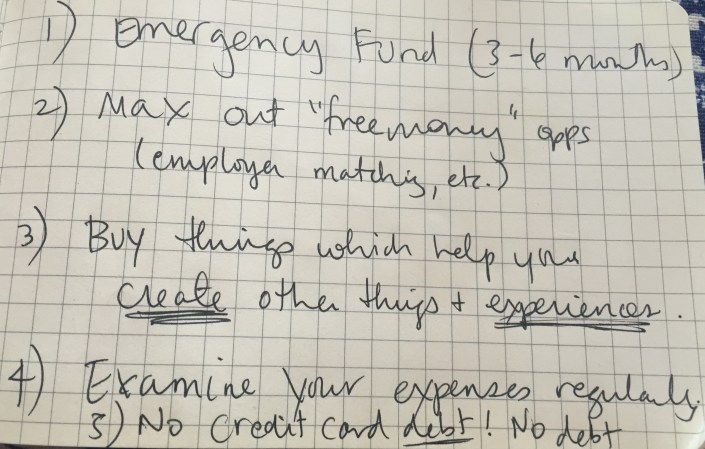

Create an Emergency Fund.

An emergency fund is an amount equivalent to 3-6 months of your expenses (rent, food, other) that will allow you to have a cushion in the event of an emergency. 3 months is minimum, 6 months is better, and I consider it the new “balance zero” when I look at my bank account.

If you don’t have an emergency fund saved up, I think you’re borrowing from yourself with every other purchase you make. An emergency fund can allow you to not have a plan for a few months, to lose a job or to find a new job with a cushion, or just to be ready for when something expensive breaks down or your life takes a turn.

The premise of an emergency fund is definitely related to the recent chatter about a “F-Off Fund” and what some are calling “financial self-defense” and I like the connotation. Having an emergency fund is good self-defense.

Resources:

- Dave Ramsey’s 7 Baby Steps (Step 1 & 3 are about emergency funds).

- A Story of a F-Off Fund (and an interesting counterpoint The Problem With The “F*ck Off Fund” No One Is Talking About)

Also related from me is my article about (financial and more) independence for women in: To My Girlfriends: How to be an Independent Woman in a Relationship including more advice and links.

Never say no to free money (aka especially from your boss / company).

Retirement matching? Subsidized benefits or other perks? Make sure you’re maxing out what’s already being offered to you. When I was 22 starting work full-time, I maxed out both my 401k matching from HP as well as the matching/discount on the stock purchase plan. At 22 retirement felt really far away, and even the stock I bought I promised to keep “until I was 30” in order to keep from selling it all, and here I am, many years later, glad that I started putting something away.

Think of your retirement matching like an instant raise and that makes your investments even more valuable — they have to drop 50% in value before they even start losing ‘your’ money.

Resources:

- The No. 6 eternal truth of personal finance: Never say no to free money from the boss

- American Employees: Are You Leaving Money On The Table?

Buy things which help you create other things and experiences.

The above can be read two ways — things which create other things and experiences, and things which create other things, and experiences. In any case, creating and experiences are key.

When I started blogging about food and travel more than ten years ago, I didn’t really have the money for a DSLR camera, but I wanted to learn more about photography and therefore made it a priority to spend money on one. The investment was returned and then some, as I ended up not only taking pictures for my own website, but selling photographs to The Wall Street Journal and La Cucina Italiana as well as some other outlets through Getty, and I was able to photograph several friends’ weddings and take numerous portraits of people and places I loved.

Now I prioritize buys which will help me create something else, or develop or explore a skill, especially those I can use offline. I’m also investing in technology and gadgets because I will learn more about how they work and why they’re interesting to us. Remember that time I ended up on WIRED Italy because I was one of the first in Italy to have an iPad? Yeah, me neither, but sometimes early adoption can unexpected (positive) side effects. 🙂

There isn’t an ‘only‘ in that statement on purpose. It’s more about prioritizing those things above other things and saying no perhaps to those which don’t immediately add much. But I always leave room for joy. Coffee cups and espresso bring me joy, so I buy little coffee cups which I use pretty much every day. That’s an experience in a way. 🙂

Everyone pretty much agrees on experiences (& joy!) vs. things, but in case you need more food for thought:

- Buy Experiences, Not Things

-

The Science Of Why You Should Spend Your Money On Experiences, Not Things

Examine your expenses regularly.

Do you know where your money is going? Really? It’s a really good exercise to set a budget for yourself and see where your money is going, even for a few months. I have used YNAB (You Need a Budget) software to track and plan my spending, and it’s been fascinating to look through spending habits and to see where things end up at the end of the month, as well as embracing one of their fundamental concepts of “giving every dollar a job.”

The “giving every dollar a job” concept has been great to stop thinking of “leftover” money as “free” and make sure you’re allocating pretty much everything you get to something, whether it’s for next month’s expenses, towards an upcoming larger expense (like replacing an appliance), or even just “allocating” it to savings or gift giving (something which most of us never set aside money for!)

You can examine your expenses in a lot of ways, and one of the ways I like to keep tabs on what I’m spending is by not using cash very much, or at all. That way, I can use my credit card statements (I’ll get to credit cards next) to track spending in categories and easily export the transactions into another tool to categorize and analyze them.

Related to that, did you know you can figure out how much money you’ve spent at Amazon over the years? The orders summary is not entirely accurate; I opened my account in 1997 and purchased then but it doesn’t let me download back that far (only until 2006), so your mileage may vary.

No credit card debt. No credit card debt. None.

For the love of yourself, please don’t run up a credit card bill. If you’re using one, make sure you’re paying it off in full every month and aren’t carrying a balance. If you don’t have enough money to pay off your bill every month, examine those expenses in the previous step, give those ‘leftover’ dollars a job of paying off that credit card, and why not try moving to a cash-only system for a while?

When I had very little money and wasn’t able to save anything when I first moved to Italy (though I had paid off my credit card debt), I got some letter-size envelopes and labeled each one “Groceries,” “Eating Out/Entertainment,” “Rent,” and “Utilities/Phone.” It was a super simple filing system, but every time I got paid, I counted out the bills and filled up each envelope with what I agreed was appropriate for that month/period. When I ran out of “Entertainment” money, I couldn’t eat out anymore and had to cook at home with friends. It was easy not to overspend because the envelopes did not refill themselves.

Bonus Tip: Invest in Passive / Index funds and avoid Active / Managed Funds.

Years ago I moved all of my previous 401k funds into index funds, and continue to seek out passively managed funds if index funds aren’t available in retirement options. This book Millionaire Teacher talks more about why you should be doing this as well (and is a good read), but John Oliver did a really good segment on this just this past week, so he sums up how & why so much better than I could. Give it a watch:

Some last advice I liked: Save even a little bit, starting now.

“I would rather see you save $10 a week than have you throw up your hands and say ‘I can’t save anything.’ It’s a good habit to get into.” — Helaine Olen [ref]

The article which inspired it all: How Should You Manage Your Money? And Keep It Short on the New York Times. Write your own financial advice on an index card and share it here and/or with someone you care about! Would love to hear what makes it onto your list.

Disclosure: Some links may have an affiliate code added, which means you help support this site at no additional cost to you! Thank you!

Share this:

Categories: Productivity, Self & Finance

I would add the 6th point: “Wait 5 days with your “needed” purchase of the next thing”. It makes magic 🙂

Nice, so spacing out ‘required’ / ‘needed’ purchases to make sure you really need them?

Exactly – suddenly it appears that after a week the new gadget that was absolutely necessary is not so important anymore and life can go on without it.

Thank you Sara! Your tips will be very useful. Grazie!

Glad you find them helpful!

Great tips Sara, I am currently doing this MooC https://courses.edx.org/courses/course-v1:MichiganX+FIN101x+1T2016/info which helping with the fundamentals.